Should I buy Nvidia stock at $221? (5 honest reasons Wall Street is asking it wrong)

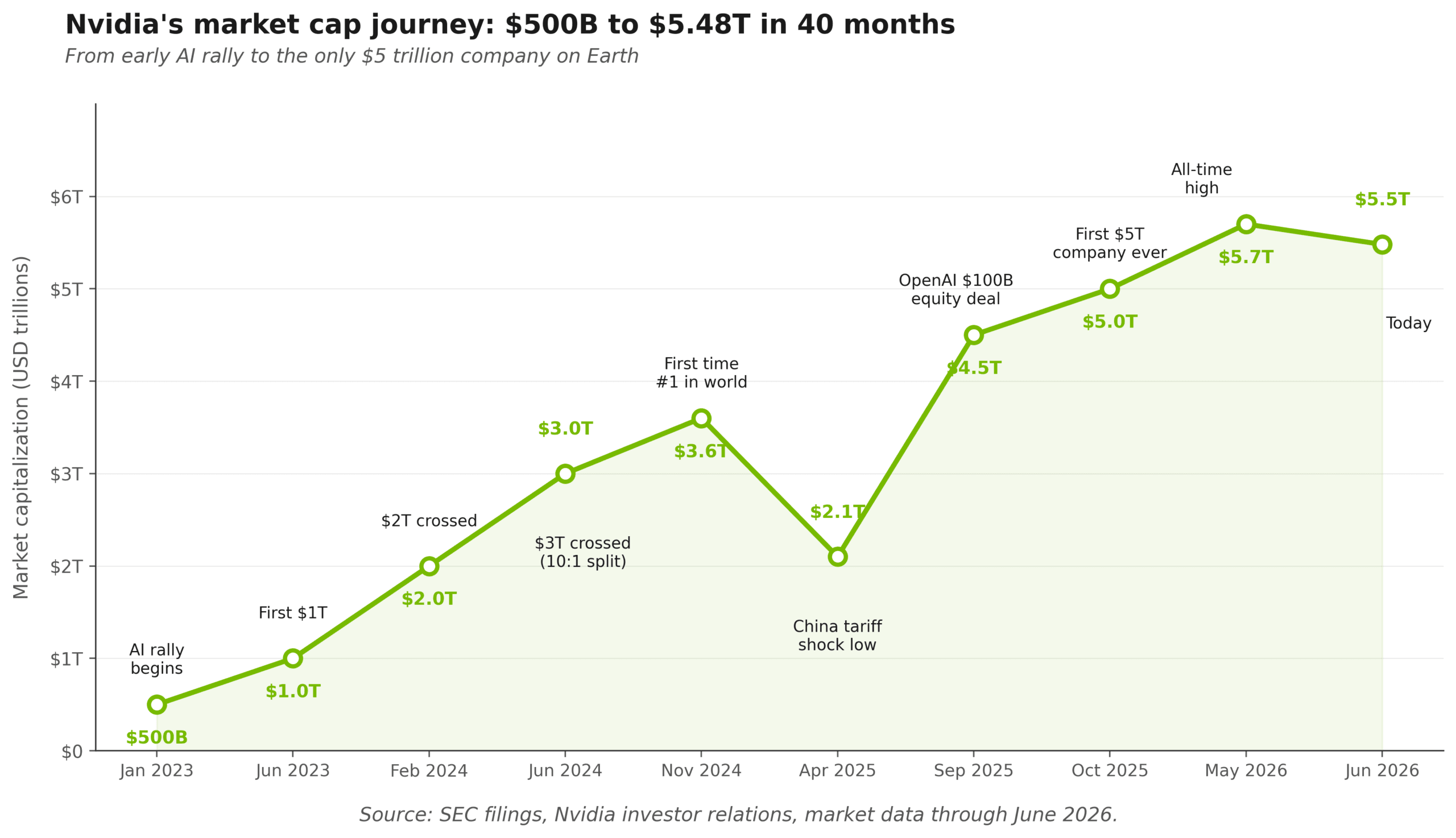

On May 14, 2026, Nvidia stock closed at $235.74 and crossed a market cap of $5 trillion. Only one company in human history has ever been worth that much.

A week later, Nvidia raised its dividend by 2,400 percent (from one cent to 25 cents per share). The same day, it authorized an $80 billion share buyback. The stock dropped anyway.

If you’re sitting on the sidelines wondering should I buy Nvidia stock now, you’re not asking the wrong question. You’re asking the question wrong.

The honest question isn’t “is Nvidia a great company?” It is. The honest question is whether “great company” equals “great buy” when you’re showing up after a 20x run.

What follows is the math, the bull case, the bear case, and a clean framework for deciding how much Nvidia stock to actually own.

What buying Nvidia stock at $221 actually means

Here’s the part most posts skip. Nvidia is currently the largest company on Earth by market cap (the total dollar value of every share outstanding). At roughly $5.48 trillion, it is worth more than the entire Indian economy.

When you ask should I buy Nvidia stock today, you are not asking what people asked in 2023. In June 2023, Nvidia first crossed $1 trillion. Someone who bought $10,000 of NVDA at that exact moment is sitting on roughly $55,000 right now.

That math is closed.

The math you’re actually buying into looks different. For Nvidia stock to return another 5x from here, the company would need a market cap of $27 trillion. That is larger than the combined economies of every country on Earth except the United States and China.

That doesn’t mean Nvidia is a bad buy. It means the realistic distribution of outcomes is narrower than newer investors assume. The base case for the next five years probably looks like 8 to 15 percent annualized returns, not the 80 percent annualized of the last three.

Sounds boring? It shouldn’t. 15 percent compounded over a decade still doubles your money in five years.

The first honest answer to “should I buy Nvidia stock” is: yes, but expect index-beating returns, not life-changing returns. The life-changing returns happened to people who bought before you.

The bull case in 3 numbers

Forget the analyst price targets. Three numbers explain why a serious investor still owns Nvidia stock at $5 trillion.

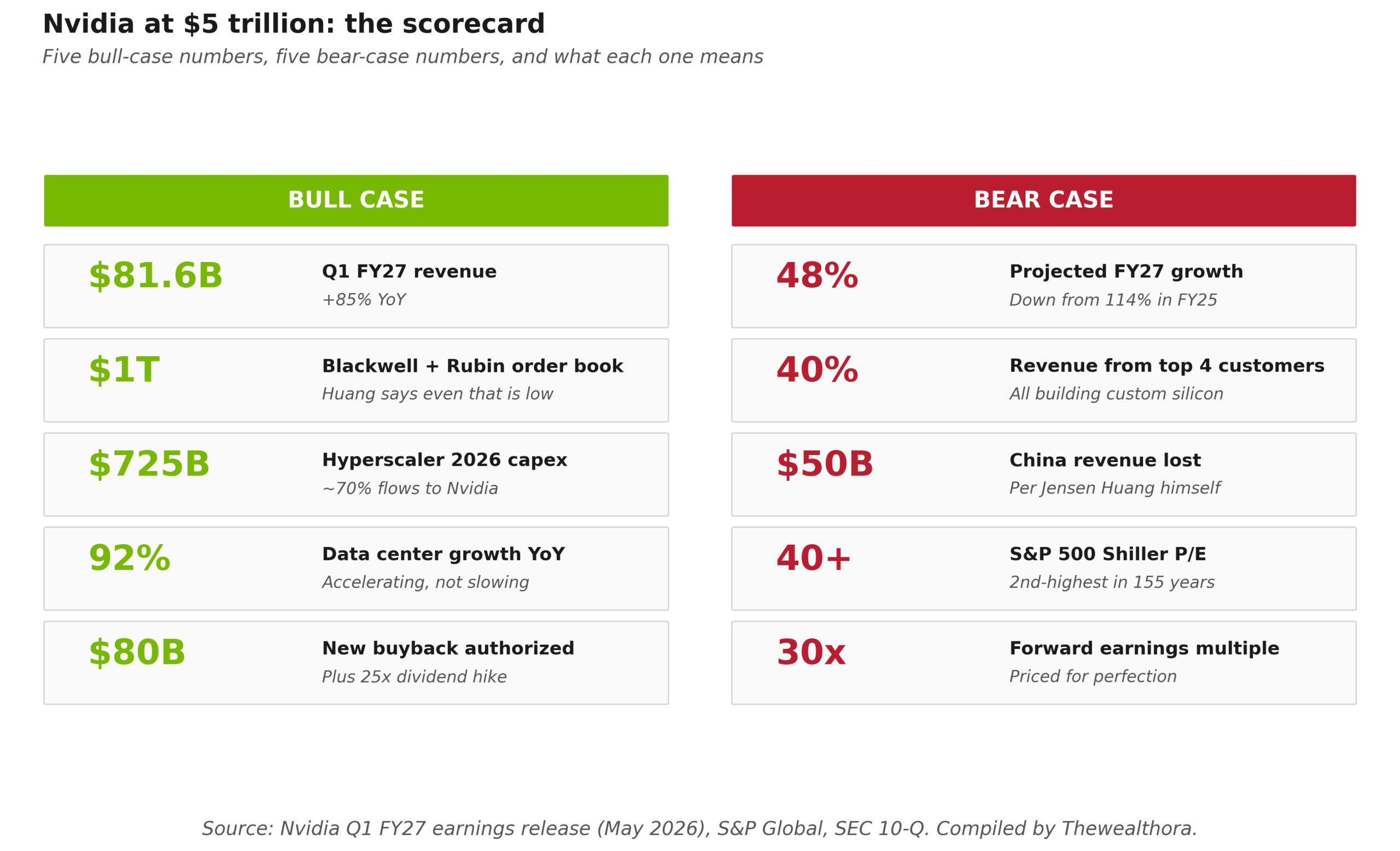

Number one: $81.6 billion. That was Nvidia’s Q1 fiscal 2027 revenue, reported on May 20, 2026. Up 85 percent year-over-year. For context, that single quarter is more revenue than Intel and AMD generated combined in all of 2025. Data center revenue alone hit $75.2 billion, growing 92 percent.

That kind of growth at this kind of scale is genuinely unprecedented in market history.

Number two: $1 trillion. At Nvidia’s March 2026 GTC conference, CEO Jensen Huang stated the company will generate “at least” $1 trillion from Blackwell and Vera Rubin chip sales by end of 2027. He added, “In fact, we are going to be short. I am certain computing demand will be much higher.” Wall Street consensus has 2-year revenue at $855 billion. Huang is saying the analysts are too conservative.

Number three: $725 billion. That is the combined 2026 capital expenditure committed by Microsoft, Amazon, Alphabet, and Meta. The number for 2027? Likely north of $1 trillion. Roughly 70 percent of every AI data center dollar flows to Nvidia.

The bull thesis isn’t subtle. AI infrastructure is the largest single capex buildout in human history, and Nvidia owns the picks and shovels.

If you believe AI is the real deal and not a 1999-style mania, then owning Nvidia stock is the cleanest direct expression of that belief in public markets.

The bear case in 3 numbers

Now the other side. Anyone telling you Nvidia stock has no bear case is selling you something.

Number one: 114, then 60, then 48. Those are Nvidia’s projected year-over-year revenue growth rates for fiscal 2025, 2026, and 2027 respectively. The growth rate is decelerating sharply. Stocks priced for perfection tend to get punished hard the first time growth misses by 5 or 10 percent. The market re-rates the multiple before you can react.

Number two: 40 percent. That is roughly the share of Nvidia revenue coming from its top four customers (the hyperscalers: Microsoft, Amazon, Google, Meta). Every one of them is actively building their own custom silicon. Google’s TPU (tensor processing unit) is now sold to third parties. Amazon has Trainium and Inferentia. Microsoft has Maia. The customers are becoming competitors. That’s a structural risk no quarterly beat fixes.

Number three: $50 billion. That is the size of the China opportunity Jensen Huang says Nvidia has lost to export controls. The Trump administration’s late-2025 partial reversal (allowing H200 chips to “approved customers”) helps, but the structural shift toward Chinese domestic chips (Huawei Ascend, Cambricon) is real.

Add the Shiller P/E (cyclically-adjusted price-to-earnings ratio) sitting at 40-plus, the second-highest in 155 years of market history, and Nvidia is being bought into a generally expensive market.

The bear case isn’t that Nvidia is a bad company. It’s that priced-for-perfection stocks get punished when reality is merely good instead of spectacular.

The 25x dividend hike nobody is reading right

This was the most underreported number from the May 2026 earnings report. Nvidia raised its quarterly dividend from $0.01 per share to $0.25 per share. That is a 2,400 percent increase. The same day, the board authorized $80 billion in additional share buybacks.

The financial press wrote it up as victory lap material. It is not.

Capital allocation is the most honest signal a CEO sends. When a hypergrowth company starts returning cash aggressively to shareholders, management is telling you something they cannot say on an earnings call: we have more cash than reinvestment opportunities can absorb.

For Apple in 2012, this signal came right as the iPhone growth-rate peaked. For Microsoft in 2003, it preceded a decade of single-digit returns. Neither company became bad. Both became boring.

This is not a sell signal. Nvidia is generating $58 billion in net income per quarter. Returning some of it makes complete sense. But the 25x dividend hike, combined with the buyback, is a quiet admission that Nvidia is transitioning from “reinvest every dollar” mode to “mature cash machine” mode.

That transition usually happens with a multiple compression (the P/E ratio falls as growth slows). Even if earnings keep growing, the price can stagnate for years while the multiple normalizes. Real math on dividend investing rarely matches the marketing pitch.

A 2,400 percent dividend hike is what late-cycle compounders do, not what early-cycle hypergrowth does. Read it as a respect signal, not a victory lap.

How much Nvidia stock should you actually own?

This is the question that matters most, and the one almost no Nvidia article answers. The decision isn’t really “should I buy Nvidia stock yes or no.” It’s “what percent of my portfolio belongs in Nvidia.”

Three reader profiles, three different answers.

Profile one: you already own VOO or VTI as your core. Nvidia is roughly 8 percent of the S&P 500 by weight. You already own it. Adding 3 to 5 percent of your portfolio in NVDA directly is reasonable. More than that and you’re heavily concentrated in one bet on one technology. If choosing between adding more Nvidia and broadening your index exposure, the VTI versus VOO decision framework matters more than the NVDA timing.

Profile two: you’re new to investing with under $5,000 to deploy. Buying a single share of Nvidia stock for $221 is roughly 4 percent of a $5,000 portfolio. That is fine. Buying ten shares is 44 percent. That is not fine. The right move for most beginners is a broad index fund first, then small single-stock positions only with money you genuinely don’t need for five years. The $25-a-week plan covers exactly this situation.

Profile three: you have an existing portfolio of $50,000-plus. The traditional rule is no single stock above 5 percent of total holdings. Some investors stretch this to 10 percent for high-conviction names. Beyond that, you’re not really diversified, you’re betting.

The hardest part of position sizing in Nvidia stock is the regret math. Buy too little and you’ll kick yourself if it 3x’s. Buy too much and you’ll panic-sell during the inevitable 30 percent drawdown.

The right Nvidia position size is the largest amount you could hold through a 40 percent decline without selling. For most people, that’s between 3 and 8 percent.

Should I buy Nvidia stock from the US, UK, or EU?

The mechanics differ by region and the differences matter more than most articles admit.

| Region | Easiest broker | Tax wrapper that fits NVDA | What’s different |

|---|---|---|---|

| 🇺🇸 US | Fidelity, Schwab, Robinhood | Roth IRA, traditional IRA, 401k brokerage window | Direct buy on NASDAQ. Fractional shares standard. Long-term capital gains 0 to 20 percent. |

| 🇬🇧 UK | Hargreaves Lansdown, Trading 212, AJ Bell | Stocks and Shares ISA, SIPP | Sign a W-8BEN form to drop US withholding tax from 30 to 15 percent. No UK stamp duty on US shares. |

| 🇪🇺 EU | DEGIRO, Trade Republic, Scalable Capital | German Sparplan, Irish PRSA (PEA can’t hold US stocks) | UCITS rules don’t restrict single US stocks. Most platforms charge a 0.25 to 0.50 percent currency conversion fee. |

A small thing that trips up UK and EU investors: the W-8BEN form for US stocks. It is a five-minute form that halves your dividend withholding tax. Most brokers prompt you when you open the account. If yours didn’t, ask.

For UK readers specifically, an ISA wrapped Nvidia position avoids capital gains tax entirely on UK side. The US withholding still applies, but the gains are clean. SIPP gives the same shielding for retirement.

Here’s what I’d actually do

Decide your position size before you buy. Buy half today, half over the next 90 days. Do not buy at the open on any day Nvidia just reported earnings.

That’s the whole list.

Nvidia at $221 is neither a screaming buy nor a clear sell. It is a fairly priced great company with decelerating growth and a quietly maturing capital allocation. The next five years for Nvidia stock will reward patient holders and punish anyone who can’t sit through a 30 percent drawdown without selling.

The mistake to avoid isn’t buying Nvidia. It is buying too much Nvidia because the chart looks so good in the rearview mirror that you forget what the windshield looks like.

A 20x return is a story that only feels obvious afterward.

Sources

- Nvidia Q1 Fiscal 2027 earnings press release, May 20, 2026 (SEC filing)

- Nvidia 10-Q filing, fiscal Q1 2027 (SEC filing)

- S&P Global Market Intelligence, Nvidia earnings preview, May 2026 (S&P Global)

- Nvidia analyst consensus and price targets (Public.com)

- The Motley Fool, Nvidia market cap analysis at $5 trillion (Motley Fool)

Arpit Soni

The Thewealthora desk covers markets, money and personal finance, with zero jargon and every claim sourced.