On May 1, 2026, the S&P 500’s dividend yield closed at 1.08%, near a 50-year low. (Yield = annual dividends divided by share price.) That same week, finance YouTube was full of “retire on dividend stocks passive income” videos, complete with screenshots of $4,200-a-year hauls and confident yield-trap picks.

Both things were true. They were also incompatible in a way most viewers never notice.

Most “dividend stocks passive income” advice is just total-return investing wearing a costume. You need more capital, you pay more tax, and you historically earn less.

This isn’t a hate-piece on dividends. I own SCHD myself, inside a tax-advantaged account where it actually makes sense. But the seven-truth version of dividend stocks passive income deserves to exist somewhere, with the 2026 numbers, an honest comparison, and one admission about where dividends genuinely earn their keep.

The capital you actually need (and why “$1k/month” isn’t passive)

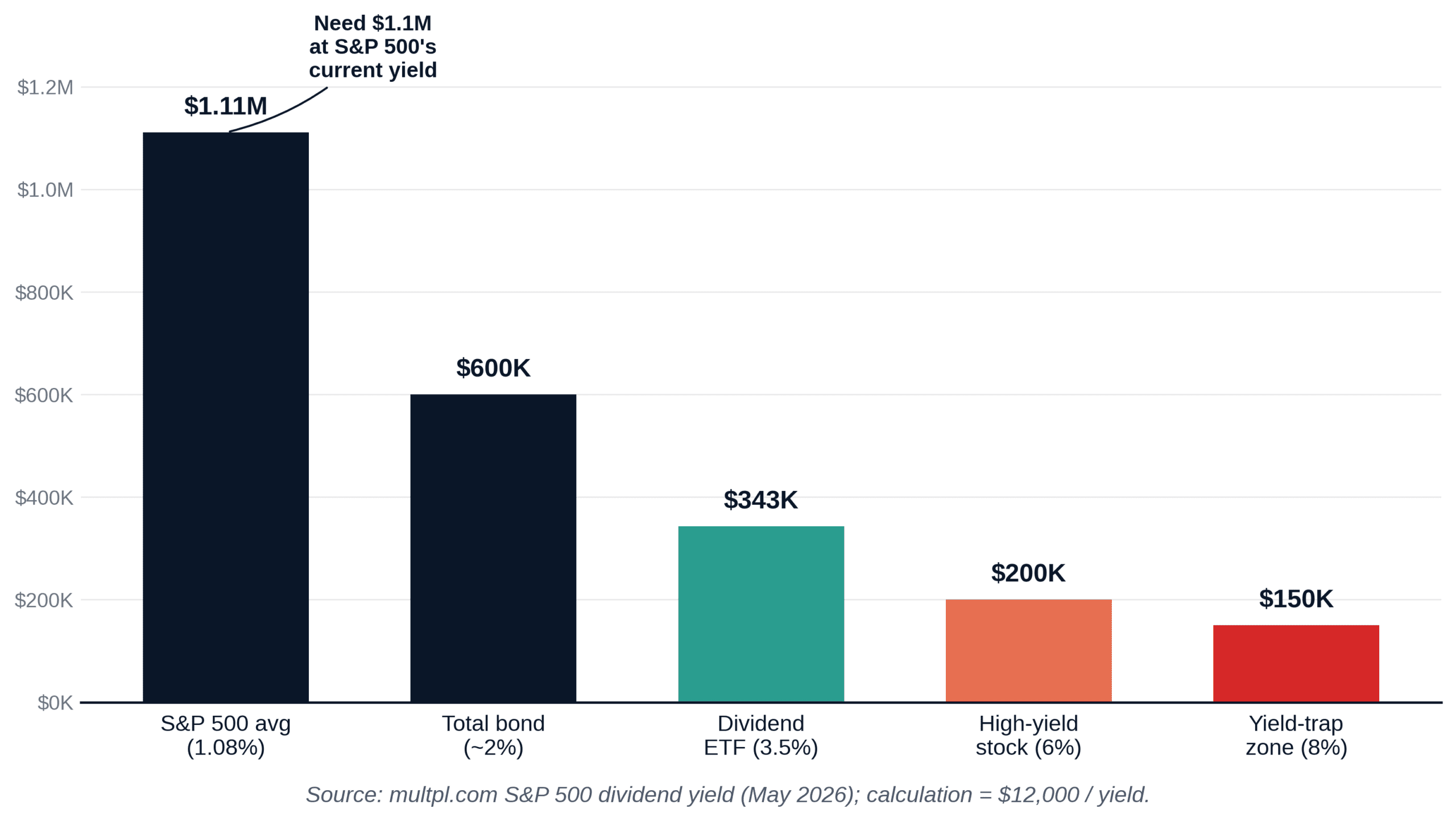

Start with the painful arithmetic. If you want $1,000 a month from dividends, that’s $12,000 a year. Divide $12,000 by your portfolio’s yield, and you get the pile required.

Plug in today’s numbers. The S&P 500 yields 1.08%, so you’d need $12,000 ÷ 0.0108 = roughly $1.11 million. A dividend ETF like SCHD pays about 3.5%, which drops the requirement to $343,000. A 6%-yielding stock like AT&T (T) gets you to $200,000. An 8% “high-yield” REIT? $150,000, but you’re picking up more risk than yield (more on that next).

The capital required scales sharply with yield, and you don’t get to choose your yield without choosing your risk. That’s the first hard truth about dividend stocks passive income most listicles dance around.

Here’s the part the listicles skip: “passive income” is the wrong frame. You don’t earn dividends. You earn the wealth required to receive them. Calling a $343,000 portfolio “passive income” is like calling a fully-paid-off rental property “free rent.” Technically true, completely misleading.

To replace a $5,000-a-month paycheck with dividend stocks passive income, you need somewhere between $1 million and $5 million invested first. The dividend isn’t the strategy. The savings rate is. If you’re starting smaller than that, I broke down a realistic build-from-zero version in my $25-a-week plan for beginners. Anyone selling you “$50 a month from $5,000” is selling you the photo, not the journey.

The dividend stocks passive income trap: why high yields are usually a warning

Scroll any “best dividend stocks 2026” list and you’ll see the same handful of names. AT&T at 6.2%. Altria at 6.5%. AGNC Investment Corp at 14%. Energy Transfer at 7%. The yields look like free money. They aren’t.

A dividend yield is a fraction. When the bottom number (the share price) drops because the market doubts the future, the yield mechanically jumps. That’s not a feature. It’s a warning light, and Wall Street has a name for it: a yield trap.

AT&T is the textbook case. Its stock went roughly nowhere from 2010 to 2024. The “high yield” was the market pricing in stagnation while management kept paying out cash they couldn’t really afford. In 2022, AT&T cut its dividend by 47% as part of the Warner spinoff. Anyone who built a “passive income” plan around it took a 47% pay cut overnight. Bank dividends were slashed in 2020. Cruise-line dividends went to zero during COVID. As one widely upvoted Bogleheads thread put it, “dividends are a micro-sale of equity with potential tax implications”.

There’s also a mechanic worth understanding. A dividend isn’t free money the company conjures up. It’s a transfer from the company’s cash pile to your account, and the share price drops by roughly the dividend amount on the ex-dividend date. (The “ex-date” is the cutoff to own the stock and receive that dividend.) You get cash, the stock loses value, the math is even before tax. Anyone evaluating dividend stocks passive income should sit with that fact for a minute.

Dividend stocks passive income vs. total return: the math no one shows you

Here’s the comparison I wish more creators did honestly. SCHD is the cleanest “quality dividend stocks” ETF on the market, 0.06% expense ratio, well-diversified. VOO is Vanguard’s S&P 500 fund, broad market, 0.03% fee. Both passive, both reinvest dividends. One chases dividend payers, one buys the index.

The 10-year scoreboard tells a clean story.

| Fund | Strategy | 10-yr annualized return | $10K grew to |

|---|---|---|---|

| VOO | S&P 500 broad market | 14.75% | $39,600 |

| SCHD | U.S. dividend equity | 12.30% | $32,000 |

| Gap | per year | 2.45 ppt | $7,600 lost |

Same period, same market, dividends reinvested in both. VOO won by roughly 2.4 percentage points a year. On a $50,000 starting position over 10 years, that gap compounds to about $35,000. On $200,000 over 20 years, it runs into six figures. That is the silent cost of a dividend stocks passive income tilt over the last decade.

This isn’t a knock on SCHD. It’s a structural reality. High-dividend strategies tilt heavily toward utilities, consumer staples, financials, and energy. They underweight the tech and growth names that drove most of the last decade’s gains: Apple, Nvidia, Microsoft, Alphabet. According to Adam Parker of Trivariate Research, “over the past 100 years the S&P 500 has averaged ~10% annual returns, with about 30% from dividends”. Note the framing. 30%, not 100%. Dividends were always part of total return, never the whole engine.

I’ll be honest about what I don’t know. I can’t tell you whether dividend strategies will outperform the broad index over the next 10 years. Nobody can. What I can tell you is that the last decade is on the public record, and the dividend tilt lost. If you’re curious about the alternative-tilt question, my renewable energy investing playbook walks through a different sector bet with the same skeptical lens.

The dividend stocks passive income tax bill, plus where it actually makes sense

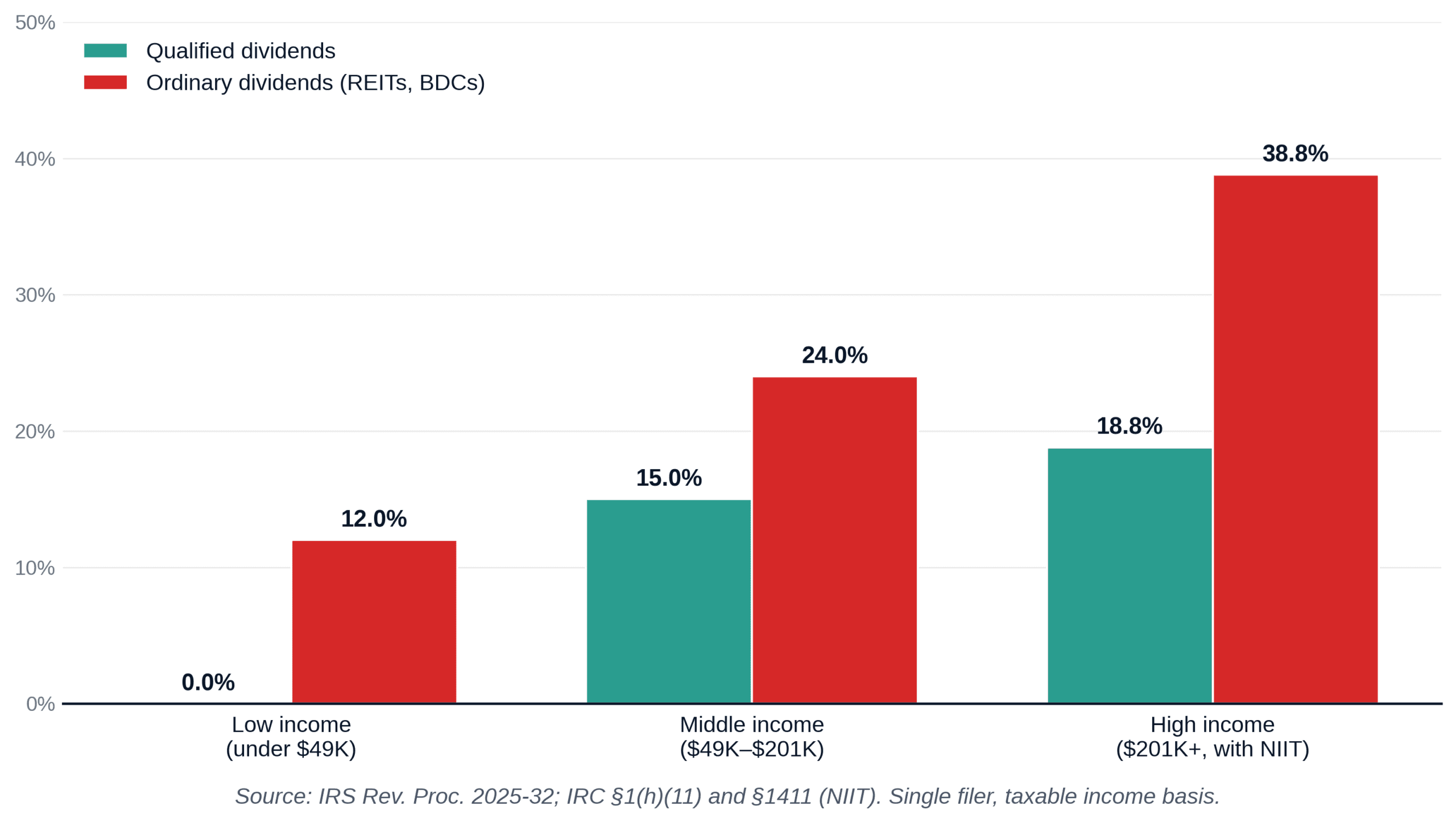

If you hold dividend stocks in a US taxable brokerage account, the IRS taxes your dividends every single year, whether you spend them or reinvest them. (Reinvestment doesn’t dodge the tax. The IRS treats DRIP-reinvested dividends as taxable income on the payment date, even though no cash hits your bank.) This is the silent leak.

Two categories matter. Qualified dividends (most US large-caps held more than 60 days) get long-term capital gains rates: 0%, 15%, or 20% in 2026, per IRS Rev. Proc. 2025-32. Ordinary dividends (REIT distributions, BDC payouts, short-held stocks) get taxed at your full ordinary rate, up to 37%. Add the 3.8% Net Investment Income Tax once your modified adjusted gross income (MAGI = AGI plus a few addbacks) crosses $200,000 single or $250,000 married, and you land at 23.8% on qualified and up to 40.8% on ordinary.

The worked example. A retired couple with taxable income under $98,900 in 2026 pays 0% federal tax on qualified dividends. A two-earner household in the 24% bracket pays $4,500 more on $50,000 of ordinary REIT dividends than on the same $50,000 of qualified ones, every single year. Same dollar amount, very different keep rate.

So where does dividend stocks passive income actually earn its keep?

Inside a Roth IRA (or UK Stocks & Shares ISA), where dividends compound tax-free forever. Strongest case by far. For retirees who need behavioral discipline, since some people genuinely cannot bring themselves to sell shares when markets are red. An automatic dividend removes the decision and the cortisol. Inside a 401(k), traditional IRA, or UK SIPP, where the annual tax drag disappears until withdrawal.

Where it actively hurts? US taxable accounts, anyone under 50 still building wealth, and anyone confusing “yield” with “return.”

The cleanest approach for most accumulators: hold a total-market fund like VTI in your taxable account, hold dividend payers inside your Roth or ISA, and ignore the dividend YouTubers entirely. If you want monthly cash later, sell roughly 0.33% of your VTI every month. Bogleheads call this a “homemade dividend.” The math equals a 4% dividend, the tax control is yours, and the IRS never forces a dividend stocks passive income payout you didn’t actually want.

Here’s what I’d actually do

Decide your savings rate. Buy a low-cost total-market index fund. Use your tax-advantaged accounts (Roth, 401(k), ISA, SIPP) before your taxable. Add a dividend tilt only if you’re inside a Roth and you genuinely value the income discipline.

That’s the whole list.

The last decade was unkind to dividend strategies because tech ate everything. The next decade may be kinder. It may not. If you do go the broad-index route, my VTI vs VOO breakdown covers which fund actually deserves your money and when VOO is the wrong pick.

The question worth asking isn’t which seven dividend stocks pay the most. It’s whether dividend stocks passive income is a strategy or a story being sold to you.

Most of the time, it’s the second one.

Sources

- Internal Revenue Service, Revenue Procedure 2025-32 (October 2025) | irs.gov

- Multpl / Standard & Poor’s, S&P 500 Dividend Yield (May 2026) | multpl.com

- Bogleheads forum, “What do Bogleheads think of passive income through dividend stocks” thread | bogleheads.org

- Stock Analysis, SCHD vs VOO 10-year total return comparison (May 2026) | stockanalysis.com

- Trivariate Research, Adam Parker commentary on S&P 500 100-year return decomposition (April 2026) | fxleaders.com

- Fidelity Learning Center, “What are qualified dividends and how are they taxed” (February 2026) | fidelity.com

Leave a Reply