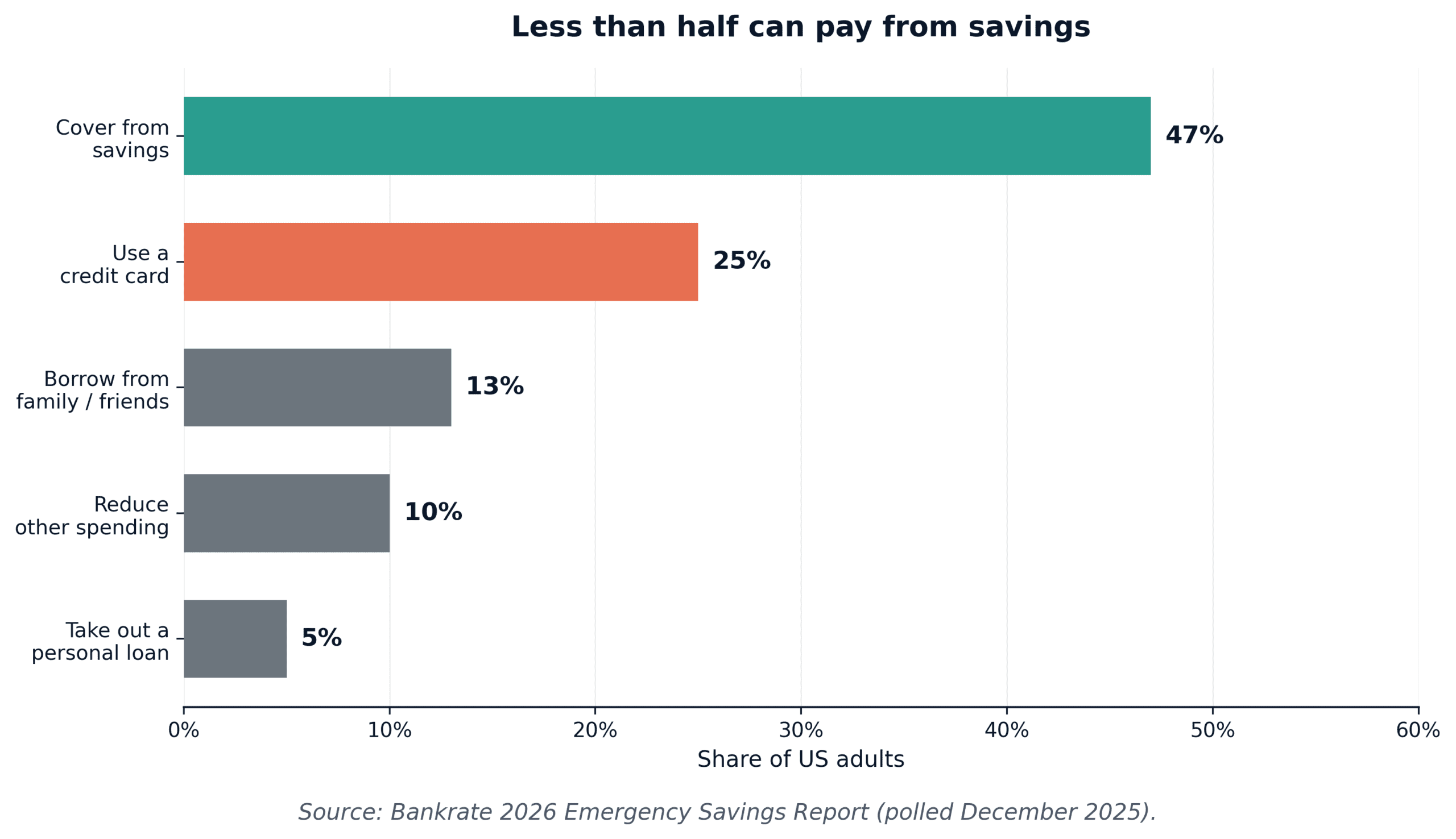

In Bankrate’s 2026 Emergency Savings Report, just 47% of Americans said they could cover a $1,000 emergency from savings. One in four had no emergency savings at all.

That’s the 2026 baseline for the country, polled in December 2025. Most lists of money habits that separate the rich will tell you the wealthy have an emergency fund. They’ll skip the part where the actual habit isn’t having one. It’s the boring monthly transfer that funded it.

The money habits that separate the rich aren’t 10 different habits. 7 of them are the same habit in different costumes. 3 actually compound.

Here’s the version with the math, ranked by what each one is actually worth.

The lie hidden in every list of money habits that separate the rich

Open any list of money habits that separate the rich from everyone else and you’ll find the same 10 bullets: live below your means, automate savings, invest early, avoid debt, track net worth, build multiple income streams, read books, hire help, buy assets, stay patient.

It’s not wrong. It’s just dishonest about how few of those are actually separate behaviors.

Tom Corley spent five years studying self-made millionaires for his book Rich Habits, and his finding was almost embarrassing in its simplicity. The wealthy automate the same boring choices and let time work. Morgan Housel makes the same point in The Psychology of Money: behavior matters more than intelligence.

The problem with the listicle format isn’t the content. It’s that it dresses up delayed gratification in 10 different costumes and sells you the costumes.

So this version ranks the actual money habits that separate the rich by what compounds, with $/£/€ math on each, the 2026 IRS and HMRC numbers that matter, and a final section on which 7 of the 10 are secretly the same habit.

Let’s take them one at a time.

The 10 money habits that separate the rich (ranked by what actually compounds)

Each habit below is small. The whole list of money habits that separate the rich is small. The hard part is doing them at the same time, for 30 years, while everyone around you doesn’t.

1. Pay yourself first (before you see the money)

Set up an automatic transfer the day your salary lands. Not the day before the next paycheck. Not “if there’s anything left.”

Vanguard’s research on 401(k) (an employer-sponsored US retirement account) behavior shows that automatic enrollment lifts participation from around 55% to 92%. The habit isn’t saving. It’s hiding the money from yourself. If you’re starting small, even $25 a week into a brokerage account becomes real over time. I walked through the math in my $25-a-week starter plan.

2. Cap lifestyle inflation at 50% of every raise

The middle-class trap is taking 100% of every raise and inflating life to match. The wealthy take roughly half, push the rest into investments, and the gap quietly widens for 30 years.

On a $5,000 raise, that’s just $208 a month invested. Over 30 years at a 7% real return, that single decision compounds to about $250,000. The Bureau of Labor Statistics’ Consumer Expenditure Survey shows almost everyone fails this one as income rises. It’s the cleanest of the money habits that separate the rich because it requires zero willpower once the auto-transfer is set.

3. Automate everything that requires willpower

Willpower is a battery, not a renewable resource. Self-made millionaires don’t have more of it. They design around it.

Direct deposit splits, auto-investing into index funds, scheduled credit card payoffs, recurring transfers to high-yield savings accounts. “What % of income do the wealthy invest?” The honest answer is 15-25%, mostly automated, never decided each month. Decisions cost willpower; defaults don’t.

4. Track net worth, ignore salary

Salary is what you bring in. Net worth is what you keep. The Federal Reserve’s 2022 Survey of Consumer Finances showed real median net worth jumped 37% from 2019 to 2022, the biggest three-year gain in modern history, almost entirely from asset ownership.

Track quarterly, not monthly. A spreadsheet works fine. Most people obsess over their salary number and ignore the only number that compounds.

5. Treat tax wrappers like a job, not a hobby

This is the entry on the money habits that separate the rich nobody actually executes. The 2026 IRS limit on a 401(k) is $24,500. The IRA limit is $7,500.

In the UK, the ISA (individual savings account) allowance is £20,000 for 2026/27, with the cash portion dropping to £12,000 for under-65s from April 2027. In Germany, the Sparplan (automatic monthly investment plan) isn’t a tax wrapper itself but pairs with the €2,000 Sparer-Pauschbetrag tax-free allowance. Every dollar that goes into one of these wrappers compounds tax-free. Every dollar outside them gets taxed twice. Once on income, once on gains.

6. Buy assets that pay you, not status that bills you

A car loan bills you every month. A dividend ETF (exchange-traded fund) pays you every quarter. The decision tree is binary, but the cultural pressure to buy the bigger car at 32 wins almost every time.

Robert Kiyosaki oversimplified it in Rich Dad Poor Dad, but the framing stuck for a reason. If you want concrete numbers on what owning a low-cost index fund actually returns over 20 years, my VTI vs VOO breakdown walks through it.

7. Build a “boring drawer” of cash before you invest a dollar

Of all the money habits that separate the rich, this is the one that feels least exciting and gets skipped most often. The instinct to skip the emergency fund and start investing is the most common Reddit mistake on r/personalfinance. Don’t.

Build 3-6 months of expenses in a high-yield savings account first. The Bankrate 2026 finding that 53% of Americans can’t cover a $1,000 emergency is what blocks them from ever staying invested through a downturn. Cash isn’t lazy. It’s what keeps you from selling at the bottom.

8. Make decisions on a 10-year clock, not a 10-day one

Every panic sell happens on a short clock. Every bull-market FOMO buy happens on a short clock. Morgan Housel writes about this constantly. The only edge most retail investors have is time horizon, and they trade it away for noise.

The renewable energy ETF crash from 2021 to 2024 was a textbook test of staying patient through a 45% drawdown, and I covered the wreckage in the renewable energy investing post.

9. Buy back time, not stuff

This is the entry in the money habits that separate the rich that breaks the pattern. The genuinely wealthy spend money to get hours back: cleaners, grocery delivery, contractors. Not because they’re lazy. Because their hours are worth more invested elsewhere.

A $50 cleaner that frees up four hours of focused side-income work is one of the best trades on the list. Dividend income works on the same logic. Your money keeps working while you don’t. I went deeper on this in the brutal truths about dividend stocks.

10. Read 30 minutes about money, every day, forever

Tom Corley’s Rich Habits research found that 88% of self-made millionaires read 30+ minutes a day for self-education. Not novels. Industry, money, biography.

The compounding here is invisible until year three. One good idea per quarter, applied consistently, beats every “guaranteed” investment newsletter. It’s the input layer for every other entry on the money habits that separate the rich.

How the money habits that separate the rich look in the US, UK, and EU

The same habit runs on different rails depending on where you live. The 2026 numbers below are the ones to actually use.

The exact mechanics of the money habits that separate the rich vary by region, but the underlying engine is identical: automate, wrap it in a tax-advantaged account, and don’t touch it.

| Region | Easy (start here) | Smart (year 2+) | Pro (year 5+) |

|---|---|---|---|

| US | Capture the full 401(k) employer match. Free money, every time. | Max the Roth IRA at $7,500. Then keep filling the 401(k) toward $24,500. | Mega-backdoor Roth or HSA (health savings account) if eligible. |

| UK | Open a Stocks & Shares ISA. Auto-pay £100 a month minimum. | Use the full £20,000 ISA allowance, plus a SIPP for higher-rate tax relief. | Lock in cash ISA before April 2027 when the limit drops to £12,000. |

| EU | Set up a monthly Sparplan (DE), PEA (FR), or ISK (SE) on a low-cost broker. | Use UCITS index funds. Avoid local funds with 1.5%+ fees. | Layer in a private pension (Riester, PERP, or country equivalent). |

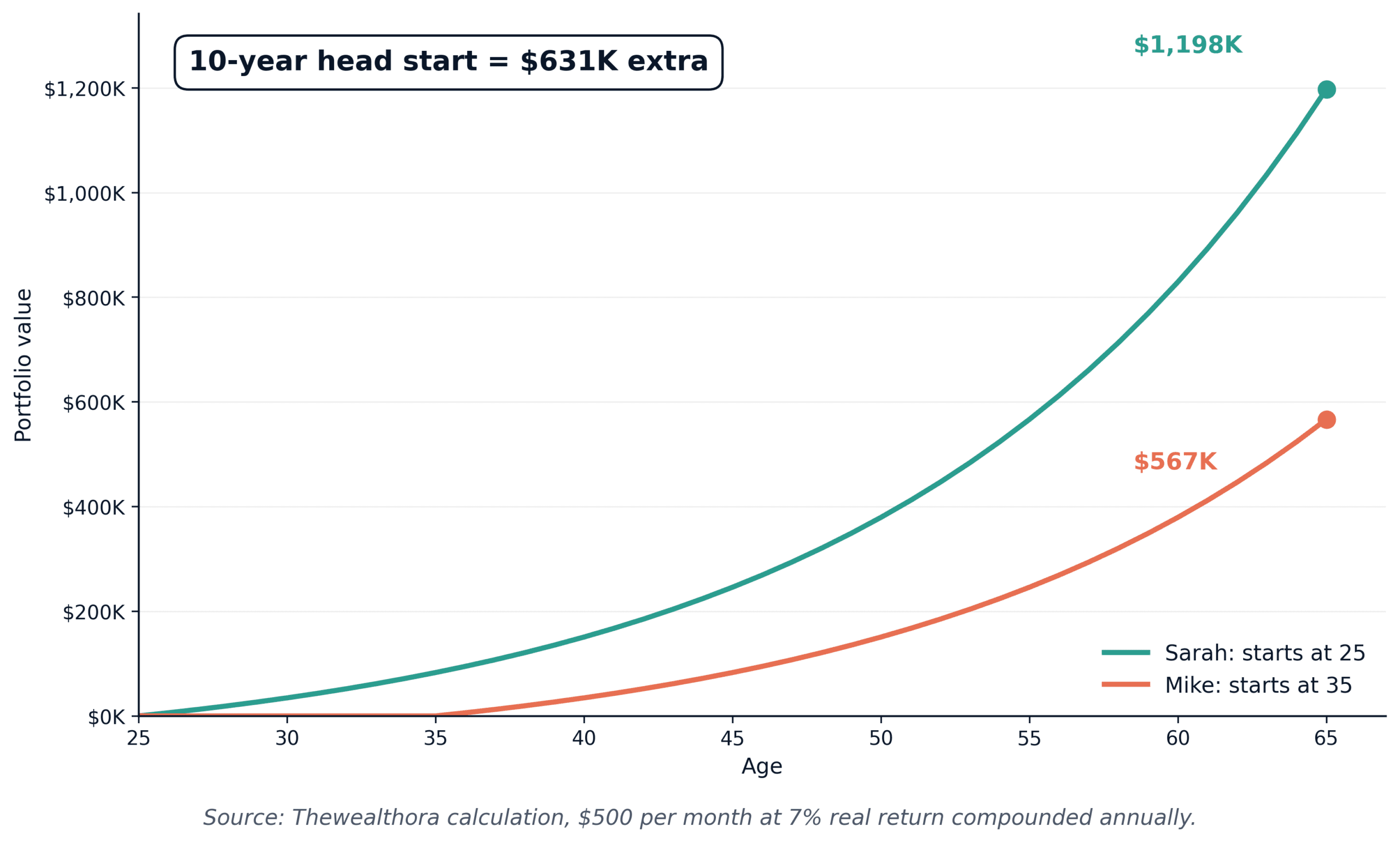

The compounding gap between starting at 25 versus 35 is what these tax wrappers are designed to capture.

In the US, the 401(k) match is the closest thing to free money in personal finance. In the UK, the ISA wrapper plus the SIPP (self-invested personal pension) handle the same job with different rules. In the EU, the picture varies by country, but Germany’s Sparplan, France’s PEA (plan d’épargne en actions), and Sweden’s ISK all pair automatic investing with tax efficiency. Same engine, different paint job, regardless of which version of the money habits that separate the rich your tax code lets you build.

The flip side of the engine is what happens when there’s nothing to buffer the bad month.

The 7 habits hiding inside one habit (and why most lists are recycled)

Look at the 10 money habits that separate the rich above. Habits 1, 2, 3, 5, 7, and 8 are all the same thing wearing different costumes: delaying consumption today so capital can compound for you tomorrow. That’s it. That’s the engine.

Habits 4, 6, 9, and 10 are the four that don’t reduce to that single move. Tracking net worth is measurement. Buying assets is allocation. Buying time is a counter-intuitive spend. Reading is input quality.

So the honest count of the money habits that separate the rich is closer to four. Plus the meta-habit. Doing those four for 30 years without quitting.

That’s also why most listicles feel hollow. They sell the costume, not the engine. I’ll admit I don’t fully understand why this insight isn’t more obvious in finance content, given how often the same writers repeat it. Possibly because “delay consumption for three decades” doesn’t make a snappy headline.

Here’s what I’d actually do

Set up one automatic transfer this week, even if it’s $50. Cap your next raise at 50% lifestyle and 50% investing. Don’t touch any of it for 10 years.

That’s the whole list.

The money habits that separate the rich aren’t a secret because the wealthy are guarding them. They’re a secret because the work is unglamorous, the timeline is long, and the win is invisible until the win is huge.

A 25-year-old who automates $500 a month at 7% real returns retires with around $1.2M. A 35-year-old doing the same retires with about $565K. The difference isn’t talent or luck. It’s a Tuesday morning decision repeated for 480 months.

That’s all the money habits that separate the rich actually are: a tiny number of small decisions, repeated for too long for anyone watching to notice when it works.

Most people will keep reading habit listicles instead of setting up the transfer.

That’s also why the gap stays a gap.

Sources

- Internal Revenue Service, 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500 (Notice 2025-67, Nov. 2025), irs.gov

- Bankrate, 2026 Emergency Savings Report (polled December 2025), bankrate.com

- HM Government, Individual Savings Account (Amendment) Regulation 2026, gov.uk

- Federal Reserve, 2022 Survey of Consumer Finances, federalreserve.gov

- U.S. Bureau of Labor Statistics, Consumer Expenditure Survey (2024), bls.gov

- Tom Corley, Rich Habits: The Daily Success Habits of Wealthy Individuals (2010), richhabits.net

Leave a Reply