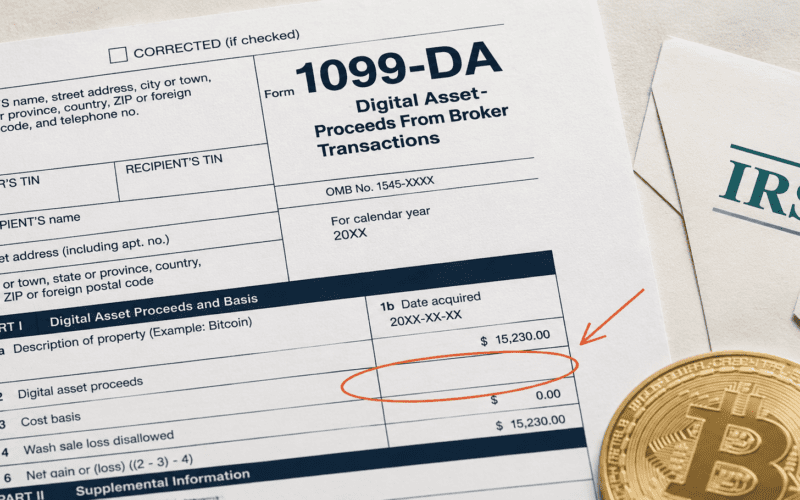

In early 2026, millions of US crypto investors will open their inbox and find a new IRS form sitting there: Form 1099-DA. It looks routine, like the 1099-INT your bank sends. It is not. For the 2025 tax year, your 1099-DA will likely show the total dollar amount you sold crypto for, with a blank box where the cost basis (the price you originally paid) should be.

The IRS is getting a copy of the same form. And if you don’t fix that blank box yourself, the IRS’s automated matching system can assume your entire sale was profit, and bill you on money you never actually made.

That is the trap. Let me walk you through it.

Your 1099-DA is not a tax bill. it’s a tripwire

Form 1099-DA stands for digital asset proceeds from broker transactions. It is the crypto equivalent of the 1099-B that Vanguard, Fidelity, or Schwab sends when you sell stocks. Coinbase, Kraken, Gemini, and Binance.US are all required to issue the 1099-DA starting this filing season for 2025 activity.

Here is the part most people miss. The 1099-DA does not calculate what you owe. It reports to the IRS what you sold for. You still have to figure out what you originally paid, subtract one from the other, and report the gain or loss on Form 8949 and Schedule D yourself.

So why does the IRS care so much about a form that doesn’t compute your gain? Because it feeds the Automated Underreporter system, the same engine that matches your W-2 against your tax return.

A mismatch between your return and the 1099-DA is the most common trigger for a CP2000 notice, the polite IRS letter that says we think you owe more, please explain.What the 1099-DA actually shows (and what it leaves blank)

For 2025 transactions, the 1099-DA you receive in early 2026 reports gross proceeds (the total dollar amount of each sale) plus the date and asset name. The IRS final regulations made cost basis reporting optional for the first year. Most brokers chose not to include it.

That means Box 1g, the cost basis box, will be blank or marked unknown for most of your 2025 trades. Holding period? Also missing in many cases. You get clean numbers on what you sold and almost nothing on what you paid.

The IRS deliberately gave brokers a grace period on cost basis reporting. Full reporting starts with 2026 transactions, so the first complete 1099-DA forms will not arrive until early 2027.

Structurally, the 2025 form is half a form. And the half it gives the IRS is the half that makes your gain look as large as possible.

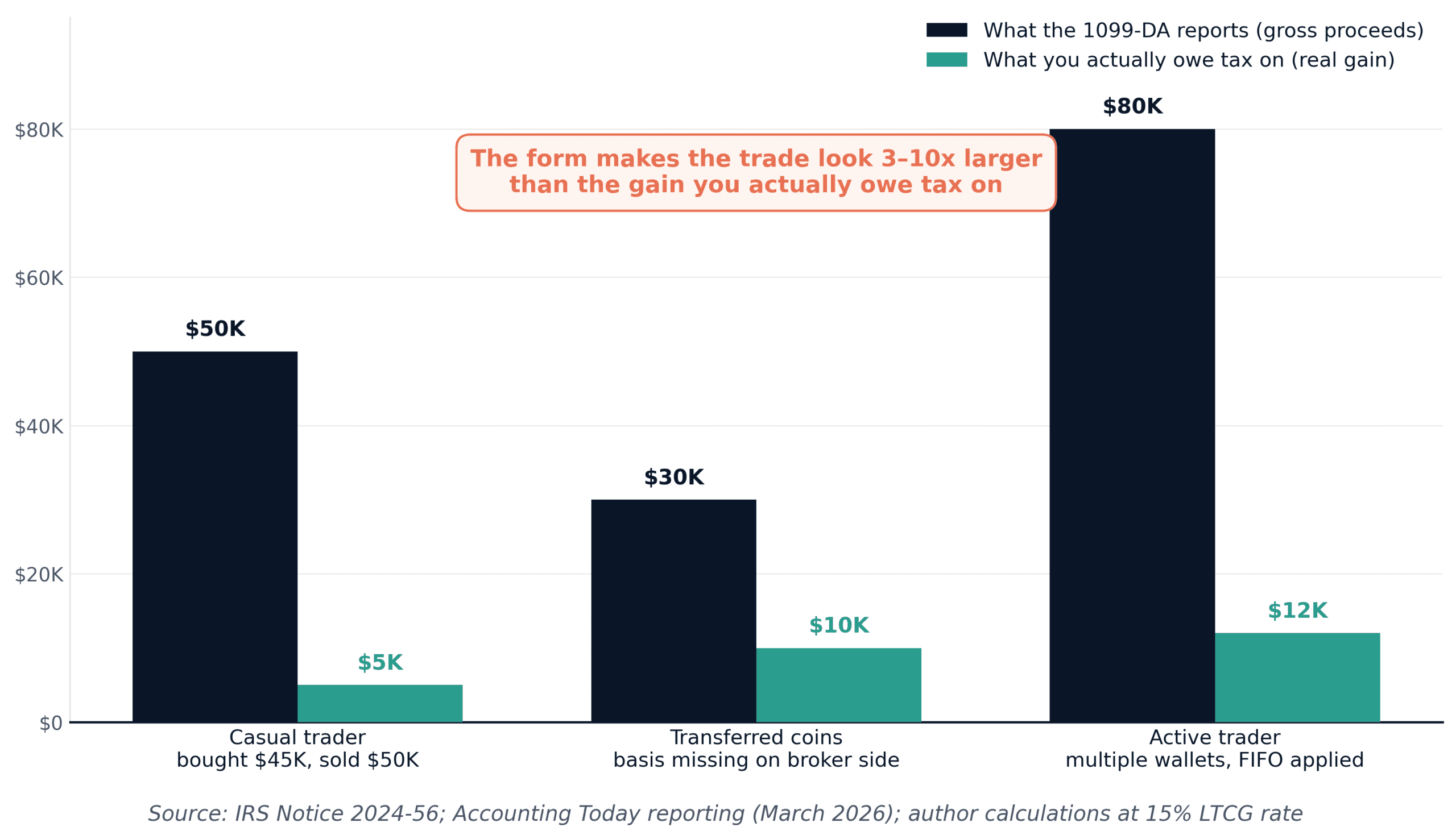

The gap between what a 1099-DA reports and what an investor actually owes tax on, across three common scenarios, looks like this.

Accounting Today called the first-year 1099-DA a rather gross problem for CPAs and clients alike. The reporting is gross like gross-of-deductions, not gross like disgusting. The effect is the same either way: the form makes you look richer than you are.

The phantom gain problem: how the IRS sees $50K instead of $5K

Imagine you bought $45,000 of Bitcoin in 2024 and sold it for $50,000 in 2025. Your real, taxable gain is $5,000. At the long-term capital gains rate of 15%, you owe $750. Done.

Now picture what the IRS receives. Your exchange files a 1099-DA showing $50,000 in proceeds. Cost basis box: blank. The matching system pulls your return and compares. If you reported the trade correctly on Form 8949, no problem. If you forgot, or filed before the form arrived, or copied $50,000 as your gain because the form did not show basis, the IRS will assume the worst.

At a 15% long-term rate, that turns a $750 bill into a $7,500 bill. Plus interest. Plus possibly an accuracy-related penalty.

That is the 1099-DA phantom gain. It does not exist in reality, but it can exist on paper until you fight it. Fighting a CP2000 letter is not a five-minute job.

Why your transferred coins might look like 100% profit

It gets worse. If you bought Bitcoin in a self-custody wallet years ago and transferred it to Coinbase to sell in 2025, Coinbase may have no idea what you paid. CountDeFi notes that when purchase history is missing, the form may show cost basis listed as unknown.

Unknown means $0 in the IRS matching system. A $50,000 sale with a $0 basis looks like a $50,000 gain. The tax on that, at typical rates, can hit $7,500 to $18,500 depending on your bracket. Against a real gain of $20,000 (if you bought in at $30,000), that is a 50% to 100% overstatement.

Self-custody users and anyone who moved coins between exchanges before 2026 are the most exposed group. The broker simply does not have your full purchase history.

This is not hypothetical. Tax preparers reported throughout the 2026 filing season that reconciling missing or zero basis was the single biggest source of extra billable hours. If you get a 1099-DA with a blank or zero basis box, don’t panic. But don’t file with those numbers either.

The wallet-by-wallet rule almost nobody followed in 2025

There is a second trap most posts skip entirely. On January 1, 2025, the IRS quietly killed the universal wallet method, which was how many crypto investors had been tracking cost basis until then.

Under the old approach, you could pool all your Bitcoin regardless of which wallet or exchange held it, and pull basis from anywhere when calculating gains. Under IRS Revenue Procedure 2024-28, each wallet now has to be treated as its own separate ledger. The default method is FIFO (first in, first out), applied wallet by wallet.

Think of it like Netflix versus a shared password. Old rules: one big pool, everyone pulls from the same balance. New rules: every wallet is its own account, with its own first-in coins, its own basis, its own audit trail.

The IRS offered a one-time safe harbor: if you allocated your pre-2025 unused basis to specific wallets by December 31, 2024, and kept written records, you were protected from penalties for misallocation. Most retail investors never knew this existed. I include myself in that group when the rule first dropped, and I had to backfill records the hard way.

If you missed the safe harbor deadline, you can still reconstruct basis, but the IRS reserves the right to challenge your allocation. Your records need to be clean enough to defend in a notice response.

All of this matters when your 1099-DA arrives, because the form is the IRS’s first reference point. Your records are your second.

The 1099-DA is US-only. here’s what UK and EU readers face

If you are reading this from London or Frankfurt, the 1099-DA does not apply to you directly. But the global crypto reporting net is closing fast, and the same blank-basis problem is about to show up in your jurisdiction too.

The UK is rolling out the Cryptoasset Reporting Framework (CARF, an OECD-coordinated regime), which takes effect in 2026 with first reports due in 2027. The EU is implementing the same framework through DAC8 (Directive on Administrative Cooperation 8), also effective from 2026. Both work similarly to the 1099-DA: exchanges report your crypto activity to local tax authorities, and you reconcile the rest yourself.

| What you face | United States | United Kingdom | European Union |

|---|---|---|---|

| The form or regime | Form 1099-DA | CARF (OECD framework) | DAC8 (Directive 2023/2226) |

| First reporting year | 2025 activity, filed 2026 | 2026 activity, filed 2027 | 2026 activity, filed 2027 |

| Cost basis included | No for 2025, yes from 2026 on covered assets | Yes for covered assets from year one | Yes for covered assets from year one |

The pattern is consistent across all three regions: gross proceeds first, full cost basis later, and the burden of proving what you paid sits with you. If you use a US-based exchange while living in the UK or EU, you may end up in both reporting systems for the same transaction. I covered the broader regulatory shift in my recent crypto regulation roundup.

Here’s what I’d actually do before April 15

Three moves, in order, before your next 1099-DA matters.

1. Pull every transaction record you have. Exchange exports, wallet CSVs, on-chain explorer history, even old bank statements showing your original buy. The 1099-DA is a starting point, not the final answer. Your records are.

2. Use crypto tax software to fill the basis gap. Koinly, CoinTracker, TokenTax, and CoinLedger all support wallet-by-wallet tracking under Rev. Proc. 2024-28. The cost ($50 to $200 a year for most retail portfolios) is a fraction of one mismatched CP2000 letter.

3. Reconcile before you file, not after. Match your software’s gain/loss output against the gross proceeds on your 1099-DA. If they line up, file. If they don’t, fix it now. The IRS would rather see a clean Form 8949 than a clean form paired with a panicked amendment.

Records win arguments.

If you have been casual with crypto records, the next 12 months are the moment to fix it. The 2026 tax year, filed in 2027, will be the first year where brokers report both proceeds and cost basis for covered assets. Mismatches that were excusable in 2025 will look much worse in 2027. The related tax-trap angle on crypto wagering sits in my recent piece on the OBBBA gambling-loss cap, which uses the same underlying logic: the IRS sees the gross, you owe on the net.

The 1099-DA is the IRS asking for a receipt. Make sure you have one before they ask twice.

The form is a mirror. The IRS only sees what you let it show.

Sources

- Internal Revenue Service, Final Regulations T.D. 10000 on Digital Asset Broker Reporting (2024) · irs.gov

- Internal Revenue Service, Revenue Procedure 2024-28: Allocation of Basis for Digital Assets (2024) · irs.gov

- Internal Revenue Service, Notice 2024-56: Transition Relief for Form 1099-DA Brokers (2024) · irs.gov

- Accounting Today, “1099-DA Rules Have a Gross Problem in 2026” (March 23, 2026) · accountingtoday.com

- The Tax Adviser, “Navigating the Form 1099-DA Reporting Maze” (March 2026) · thetaxadviser.com

- OECD, Crypto-Asset Reporting Framework (CARF) Implementation Guidance (2025) · oecd.org

Leave a Reply