Best stablecoin to invest: 3 safe options the new law just reshaped

On 11 March 2023, a coin that was supposed to be worth exactly $1 traded for 87 cents. It was USDC, the second-biggest stablecoin on earth, and for one weekend it behaved like anything but stable. If you are hunting for the best stablecoin to invest in, that single day matters more than any glossy ranking, because it shows what these things actually do when the system cracks.

Here is the part the listicles bury. A stablecoin is engineered to never move. It is pegged to $1 on purpose (pegged means its value is locked to a reference asset, usually the US dollar). So picking the best stablecoin to invest in is not about chasing gains. It is about which one holds the line, how the new law changed the rules, and whether the coin is even legal where you live.

That last point is what almost nobody tells beginners. The best stablecoin to invest in for an American is not the same one a German or a Brit should touch in 2026, and the reason is a stack of laws that landed in the last twelve months.

Why “best stablecoin to invest” is the wrong question

Most people arrive at stablecoins expecting a yield machine. You park dollars, you earn interest, the number goes up. That mental model is now mostly illegal in the US, and it was always the riskiest way to think about these coins.

A stablecoin is closer to a digital dollar in your pocket than to a stock. You do not buy one hoping it climbs to $1.20. You hold it because it sits still while everything else in crypto lurches around. Think of it like the cash drawer at a busy restaurant. The drawer is not where you make money. It is where you keep money safe between the moves that do.

So when someone asks for the best stablecoin to invest in, the honest reframe is: which coin will still be worth $1 next Tuesday, and which one is allowed to exist on your exchange. I went down this same road comparing tokens that promised the moon in my XRP breakdown, and the lesson repeats here. The boring question is the profitable one.

What actually keeps a stablecoin glued to $1

Not all stablecoins are built the same way, and the design decides how badly it breaks under pressure. There are three families worth knowing before you pick the best stablecoin to invest in.

Fiat-backed coins hold real dollars and short-term US government IOUs in a bank, one dollar of reserves for every coin issued. USDC and USDT work this way. Crypto-backed coins like DAI lock up other cryptocurrencies as collateral, usually more than $1 of crypto for every $1 coin, to absorb the swings. Algorithmic coins hold almost nothing real and try to hold the peg with code and incentives.

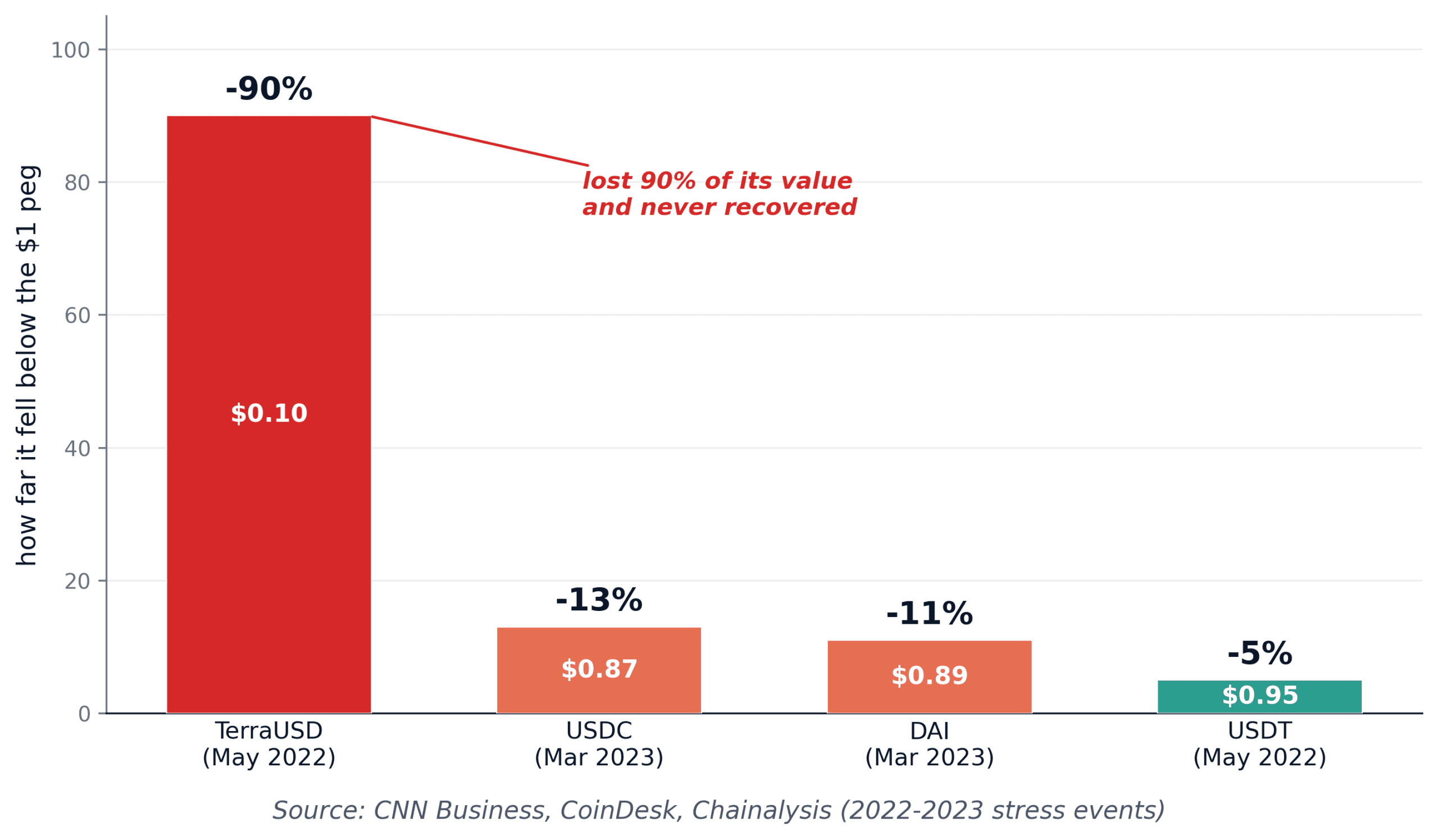

That third type is where fortunes died. In May 2022, TerraUSD, a purely algorithmic coin, fell from $1 to around 10 cents in days and wiped out roughly $40 billion. It never came back. As of early 2026 the total stablecoin market sits above $300 billion, and the survivors are almost all fully backed by real assets.

The takeaway is blunt. If a coin cannot show you the cash and Treasuries behind it, it is not a contender for the best stablecoin to invest in. It is a science experiment, not a savings tool.

The 3 stablecoins actually worth holding, ranked by safety

Strip away the noise and three names do almost all the real work when you are deciding on the best stablecoin to invest in. Together, USDC and USDT alone make up more than 80% of the entire stablecoin supply as of January 2026.

USDC (issued by Circle) is the trust pick. It publishes monthly reserve reports verified by an accounting firm, and it moved early to comply with both US and European rules. USDT (Tether) is the liquidity king. It is the most traded coin in all of crypto, accepted nearly everywhere, though some investors still grumble about how transparent its reserves really are. DAI (run by the MakerDAO community) is the decentralized option, fully on-chain and not controlled by a single company, which appeals to people who do not want a corporation holding the keys.

One regular on the r/CryptoCurrency forums put the consensus plainly: “USDC to sleep at night, USDT to actually trade.” That single line captures the trade-off better than most paid research. If you want the safest store of value, USDC leads. If you want the deepest market and instant acceptance, USDT wins on reach.

I will admit the honest gap here. I cannot tell you Tether’s reserves are bulletproof, because Tether has never given the public a full audit to the standard a bank faces. It has processed billions in redemptions without failing, which counts for a lot. But “never broken yet” is not the same as “proven safe,” and anyone who tells you otherwise is selling something.

The best stablecoin to invest in changes the moment you cross a border

This is the section that should reshape how you choose. The best stablecoin to invest in genuinely depends on which passport you hold, because three big regions now enforce very different rules.

In the US,

the GENIUS Act was signed into law on 18 July 2025, the first federal stablecoin law in the country’s history.It forces issuers to hold 1:1 reserves in cash and Treasuries and publish monthly disclosures.

In the EU, the MiCA framework set a hard deadline of 1 July 2026 for issuers to get authorized, and coins that miss it get delisted from regulated European exchanges.The UK’s Financial Conduct Authority is rolling out its own rules along similar lines.

The real-world effect is already visible. Tether’s USDT has not secured EU authorization, so regulated European platforms have been pulling it. Binance delisted USDT spot pairs for European users on 31 March 2025, and Kraken moved it to sell-only. USDC, which got its European license, kept trading. I traced this whole regulatory wave in what actually changed in 40 days, and stablecoins sit right at the center of it.

Here is how the picture breaks down by region.

The same coin can be the smart choice in one country and a dead end in another.

| Region | Easy pick | The rule that decides it |

|---|---|---|

| US | USDC or USDT | GENIUS Act demands 1:1 reserves and bans issuer-paid yield |

| UK | USDC | FCA rules favor authorized, fully backed issuers |

| EU | USDC or EURC | MiCA delists unauthorized coins from 1 July 2026; USDT already pulled |

The yield trap: why “27% stablecoin interest” should scare you

Search for the best stablecoin to invest in and you will trip over ads promising 15%, 20%, even 27% returns on something that is supposed to just sit at $1. Stop and read that twice. A dollar cannot safely pay you 27% to stay a dollar.

The GENIUS Act made this explicit.

It bans issuers from paying any interest or yield directly to stablecoin holders.The reasoning is clever: if a coin paid you for holding it, that “expectation of profit” could legally turn it into a security, with all the regulation that brings. So Washington cut the cord.

But the high numbers did not vanish. They migrated to synthetic coins like USDe, which generates returns through complex hedging trades in the derivatives market rather than sitting in a bank. Some staked versions advertised yields near 27%. That return is real, but so is the machinery behind it, and machinery breaks. A 27% yield is the market screaming “this is not a savings account.”

What about earning yield through an exchange instead? That loophole exists. Circle pays a slice of its interest to Coinbase based on USDC balances held there, and the exchange can pass rewards to you. It is legal for now, but the OCC (Office of the Comptroller of the Currency, a US banking regulator) proposed tightening it in February 2026. Treat any stablecoin yield as a temporary feature, not a guarantee. If you want a sense of how these on-chain income products actually reach retail, or fail to, I unpacked it in the on-chain bonds guide.

The $0.87 day: what the USDC depeg teaches every holder

Back to that March 2023 weekend. Circle revealed that $3.3 billion of USDC’s reserves, about 8% of the total, were stuck in the collapsing Silicon Valley Bank. Holders panicked, redemptions flooded in, and USDC fell to 87 cents before the US government guaranteed the bank’s deposits and the coin snapped back to $1 within three days.

Nobody lost their dollar in the end. But for a weekend, the safest, most transparent, most regulated stablecoin on the market was worth 13% less than it promised. That is the lesson the rankings skip.

Even the best stablecoin to invest in carries counterparty risk (the chance that a bank or company holding your money fails). The coin is only as solid as the institutions behind it. This is why spreading meaningful cash across more than one issuer beats betting everything on a single name, no matter how clean its reports look.

A worked example. Say you park $10,000 in stablecoins as a crypto cash buffer. Splitting it $6,000 in USDC and $4,000 in USDT means a single issuer stumble dents part of your stack, not all of it. During the 2023 scare, a holder fully in USDC watched their entire balance wobble. A split holder slept better.

Here’s what I’d actually do

Hold USDC as your core for safety and clean reserves. Add USDT only if you trade often and need its reach. Skip anything promising double-digit yield on a dollar.

That’s the whole list.

The best stablecoin to invest in is not a treasure hunt. It is a safety decision dressed up as an investment question, and the boring answer usually wins. Match the coin to your region first, check that real assets back it second, and ignore the yield sirens third.

Stablecoins are the cash drawer, not the meal. Keep the drawer trustworthy, and let the rest of your money go do the actual cooking.

Stable is the whole point. Anything that pays you to forget that is quietly charging you for the privilege.

Sources

- U.S. Congress / GENIUS Act of 2025 (Public Law) / congress.gov

- The White House, Council of Economic Advisers, Stablecoin Yield Prohibition (2026) / whitehouse.gov

- CNN Business, USDC breaks dollar peg after SVB exposure (2023) / cnn.com

- CoinDesk, USDC regains dollar peg after Silicon Valley Bank chaos (2023) / coindesk.com

- European Securities and Markets Authority, MiCA stablecoin authorization (2024-2026) / esma.europa.eu

- Congressional Research Service, The Stablecoin Yield Debate (2026) / congress.gov

Arpit Soni

The Thewealthora desk covers markets, money and personal finance, with zero jargon and every claim sourced.