In March 2026, the average US household spent $6,224 a year on food at home, per the Bureau of Labor Statistics. A family of four on the USDA moderate plan spends closer to $895 to $1,430 a month.

So yes, the best credit card for groceries can save you real money. Maybe $200 to $400 a year. But the best credit card for groceries isn’t the one trending on every listicle. And honestly, the best credit card for groceries on paper isn’t always the one that wins your wallet.

Here’s what no listicle leads with.

The card that wins the “best credit card for groceries” headline on almost every site is really earning 4.4%, not the 6% advertised, once you do the math. And it pays exactly 1% at Walmart, Target, Costco, and Sam’s Club, where roughly half of US grocery dollars actually go.

Let me walk you through the trap before the picks.

What “supermarket” actually means on your statement

Every card swipe sends a 4-digit tag to the bank called the MCC (merchant category code, the label that tells your card what kind of store this is). Grocery stores get code 5411. Warehouse clubs like Costco get 5300. Discount stores like Walmart Supercenter and Target get 5310 or 5311.

That distinction is the whole game. When a card advertises “6% at US supermarkets,” it means MCC 5411. Nothing else.

Walmart Supercenter, Costco, Sam’s Club, and most Targets all code as discount stores or warehouse clubs, not supermarkets. Your “6% on groceries” card pays 1% in all of them.

Walmart Neighborhood Market stores (the smaller food-only ones) sometimes code as 5411, but it’s hit or miss. A myFICO forum user, going to six different Walmart stores across two states, said they never once saw a Supercenter code as grocery.

This is why the best credit card for groceries question doesn’t have one universal answer. It has roughly three: one for supermarket regulars, one for warehouse-club shoppers, one for Walmart-heavy households. The best credit card for groceries that wins for a Whole Foods regular loses for a Costco family.

Pull your last three months of statements and sort by store. That number decides which best credit card for groceries fits you.

The 6% headline vs the 4.4% reality

Let’s run the numbers on the card that wins almost every best credit card for groceries listicle in 2026: the Blue Cash Preferred from American Express.

Its rate at US supermarkets is genuinely 6%. The trap is the cap: 6% applies only to the first $6,000 of grocery spending per calendar year, then drops to 1%. The card also costs $95 a year (waived the first year).

Max it out and you earn $360 in cashback. Subtract the $95 annual fee and your net is $265. Spread that over $6,000 of spending and your effective grocery cashback rate is 4.4%, not 6%.

That 4.4% number is what every honest comparison should lead with, and almost none of them do.

Spend less than the cap and the math gets weaker. At $4,000 a year of groceries, you earn $240 minus $95 equals $145 net, or 3.6% effective. At $3,000, you’re at $85 net, or 2.8%, barely better than a flat 2% card with no fee.

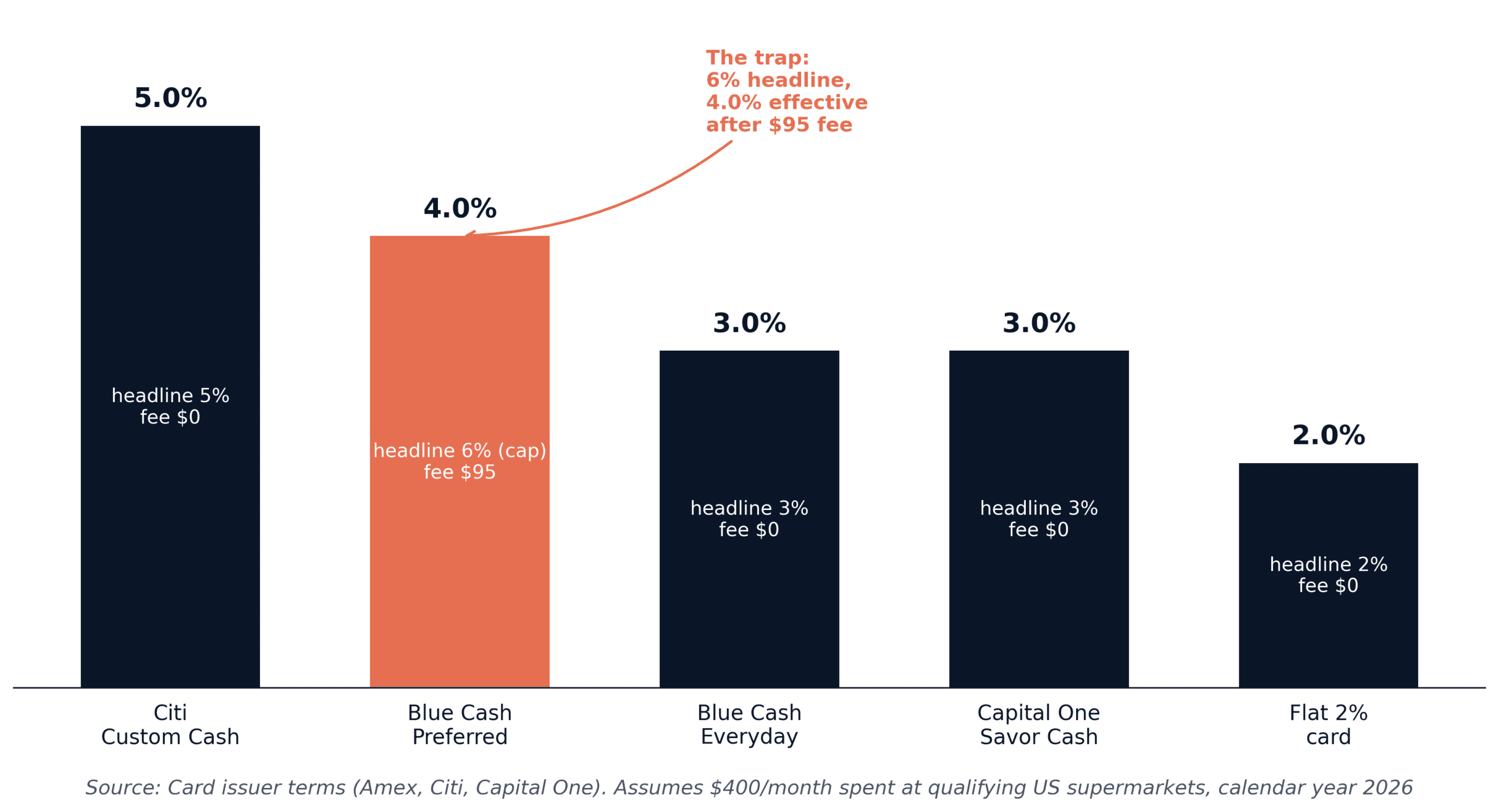

Here’s what that looks like across five popular picks at $400 a month, all at a traditional supermarket

Below $3,500 a year of grocery spend, no-fee cards win almost every time. Above $6,000, the Blue Cash Preferred pulls ahead, but only if you actually shop at qualifying supermarkets. The best credit card for groceries shifts hard at that spending threshold.

5 honest picks, ranked by who you are

Picking the best credit card for groceries is less about “which card is best?” and more about “which version of me am I?” Five clean profiles, five honest picks.

Blue Cash Preferred from American Express. For the traditional-supermarket household spending $400 to $500 a month. 6% at US supermarkets up to $6,000/year, then 1%. $95 fee after a $0 intro year. Works at Kroger, Publix, Safeway, Whole Foods, Trader Joe’s.

Citi Custom Cash. For modest spenders under $500/month. 5% on your top spending category each billing cycle, up to $500. At max, $25/month or $300/year, no fee. Monthly cap not annual, which is rare.

Capital One Savor Cash Rewards. For high-volume supermarket shoppers who avoid superstores. 3% on groceries (explicitly excluding Walmart, Target, and warehouse clubs), no cap, no fee. A household at $800/month earns $288/year.

US Bank Shopper Cash Rewards. For Walmart or Target loyalists. 6% at two retailers you select from a list (Walmart and Target are both on it), up to $1,500/quarter. $95 fee. The card most best credit card for groceries lists won’t tell you about, because the listicle template assumes you shop at supermarkets.

Prime Visa from Chase. For Whole Foods or Amazon Fresh loyalists. 5% back at both, no card fee. Requires Amazon Prime (about $139/year), so net depends on whether you’d pay for Prime anyway.

You’ll need decent credit to qualify for the premium picks. Below a 690 FICO, most of these don’t approve.

| Card | Grocery rate | Cap | Annual fee | Best for |

|---|---|---|---|---|

| Blue Cash Preferred | 6% at US supermarkets | $6,000/year | $95 (waived year 1) | $400 to $500/month supermarket spenders |

| Citi Custom Cash | 5% on top category | $500/month | $0 | Modest spenders under $500/month |

| Capital One Savor Cash | 3% (no superstores) | No cap | $0 | High-volume supermarket shoppers |

| US Bank Shopper Cash Rewards | 6% at 2 selected retailers | $1,500/quarter | $95 | Walmart or Target loyalists |

| Prime Visa | 5% Whole Foods / Amazon Fresh | No cap | $0 (Prime ~$139/yr) | Whole Foods or Amazon Fresh regulars |

What if you mostly shop at Walmart, Costco, or Target?

This is the question most best credit card for groceries comparisons quietly skip. If your grocery dollars mainly land at superstores or warehouse clubs, traditional supermarket cards are useless for you.

A few honest options.

The Costco Anywhere Visa from Citi earns 2% inside Costco (warehouse and Costco.com) and 4% at gas stations on the first $7,000/year. No card fee, but you need a Costco membership ($65/year for Gold Star). An uncapped 2% inside the warehouse is honest.

The US Bank Shopper Cash Rewards mentioned above is the strongest pick for Walmart and Target loyalists, since you can lock 6% on those two retailers.

The Capital One Quicksilver or any flat 2% card (Wells Fargo Active Cash, Citi Double Cash) is the lazy honest answer if your grocery shopping is spread across superstores, supermarkets, and warehouse clubs. 2% on everything beats 1% on the wrong card.

A flat 2% card almost always beats a 6% supermarket card if more than half your grocery spending happens at Walmart, Target, Costco, or Sam’s Club.

That’s the answer no listicle hands you, because the listicle is selling a referral.

When “best” isn’t a single card (the two-card stack)

The cleanest way to play the best credit card for groceries game in 2026 is to stop looking for one card. The best credit card for groceries for any household earning over $400 a month often isn’t a single card at all.

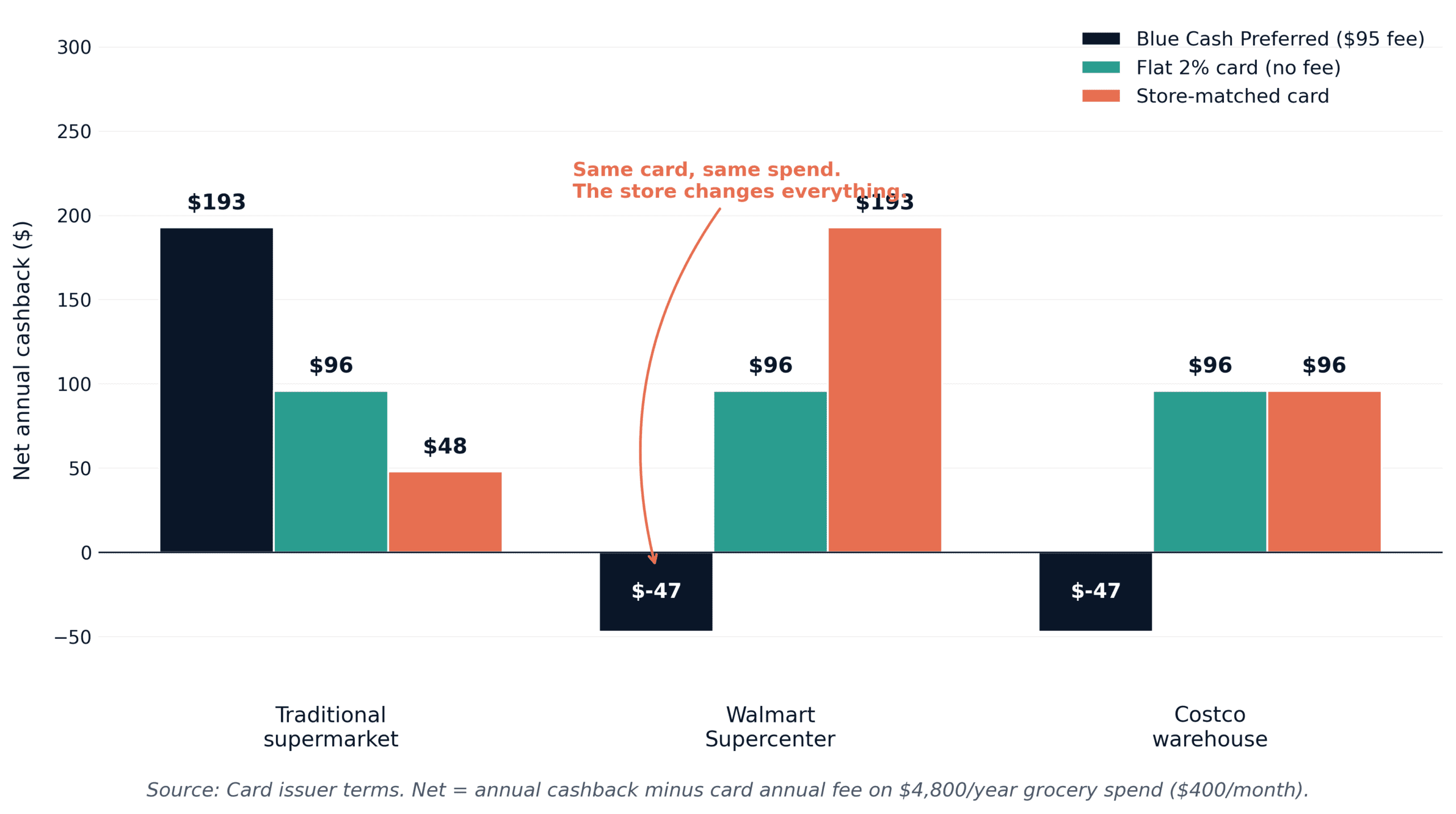

A common two-card stack: the Citi Custom Cash as your $500-a-month grocery card (5%, no fee), paired with a flat 2% card like the Citi Double Cash for everything else. Total cashback on $6,000 of grocery spending: $300 from the Custom Cash plus $20 from the Double Cash on the $1,000 overflow. Net: $320, $0 in fees.

The same stack works with the Blue Cash Everyday (3% at supermarkets up to $6,000, no fee) if you don’t want to chase the monthly cap. The chart below shows $400/month at three different store types against three card setups. The “winner” changes by store

The stack also dodges the annual fee trap that catches a lot of cashback chasers. The best credit card for groceries for most households is two no-fee cards, not one premium card.

Here’s what I’d actually do with $400 a month on groceries

Honestly? If I’m spending $400 a month at a traditional supermarket and want zero hassle, the Blue Cash Everyday is my answer. 3% at US supermarkets up to $6,000/year, no fee, works at any spend level without me tracking caps.

The best credit card for groceries for me is the one where the math still works in a bad year. A $95 fee on the Blue Cash Preferred works like a gym membership you only use twice a month. The fee runs whether you maxed the bonus or not. I’d need $1,580/year at qualifying supermarkets just to break even versus the no-fee Everyday. That’s $130 a month. Anyone under that line is paying $95 for slightly worse math.

If I were spending $700 a month and willing to do the paperwork, the Preferred wins on raw dollars. But confirm you actually shop at qualifying supermarkets, not Walmart Supercenters, first. For Walmart-heavy households, the US Bank Shopper Cash Rewards is the only card on this page that meaningfully beats a flat 2% setup.

One last thing nobody mentions. Cashback isn’t free money if you carry a balance. Average credit card APR right now sits near 21% per the Federal Reserve’s G.19 release. Earning 4.4% cashback while paying 21% interest is losing 16.6%. The best credit card for groceries only works if you pay the full statement each month.

I don’t know what your actual spend looks like. But pull your last three statements, sort by merchant, and the answer almost picks itself.

If you’re already optimizing groceries, the next move is figuring out where that $300/year goes. Cashback isn’t life-changing on its own, but funneled into something like a $25-a-week investing plan over a decade, it turns into real money. That’s the kind of move covered in my 10 money habits that separate the rich from everyone else.

The best credit card for groceries isn’t the one with the highest headline rate. It’s the one where the math works at your real spend, at your real stores, in a year you don’t max anything out.

Sources

- U.S. Bureau of Labor Statistics, The Economics Daily (January 2026), household spending on food at home and food away from home, 2024 averages, bls.gov

- USDA Food and Nutrition Service, Official Food Plans, February 2026, fns.usda.gov

- USDA Economic Research Service, Food Price Outlook, summary findings (April 2026 release), ers.usda.gov

- American Express, Blue Cash Preferred Card terms and benefits, americanexpress.com

- Federal Reserve, Consumer Credit G.19 release, commercial bank interest rates, federalreserve.gov

- WalletHub, Blue Cash Preferred supermarkets list and Walmart eligibility, wallethub.com

Leave a Reply